The Debt Tool: How to Use Borrowed

Money for Assets, Not Liabilities

"Get out of debt."

It’s some of the most common financial advice you’ll ever hear. For many, the word "debt" conjures images of stress, mounting credit card bills, and financial ruin. And for good reason—when used improperly, debt is a destructive force that can trap you in a cycle of living paycheck to paycheck.

But what if I told you that debt isn't inherently evil? What if it's just a tool—a powerful one—that can either build a prison of financial anxiety or construct a skyscraper of wealth?

The wealthiest people in the world don’t just avoid debt; they master it. They understand the fundamental difference between borrowing to consume and borrowing to invest. It’s time to flip the script and learn how to use debt not for liabilities that drain your wallet, but for assets that fill it.

The Great Divide: Good Debt vs. Bad Debt

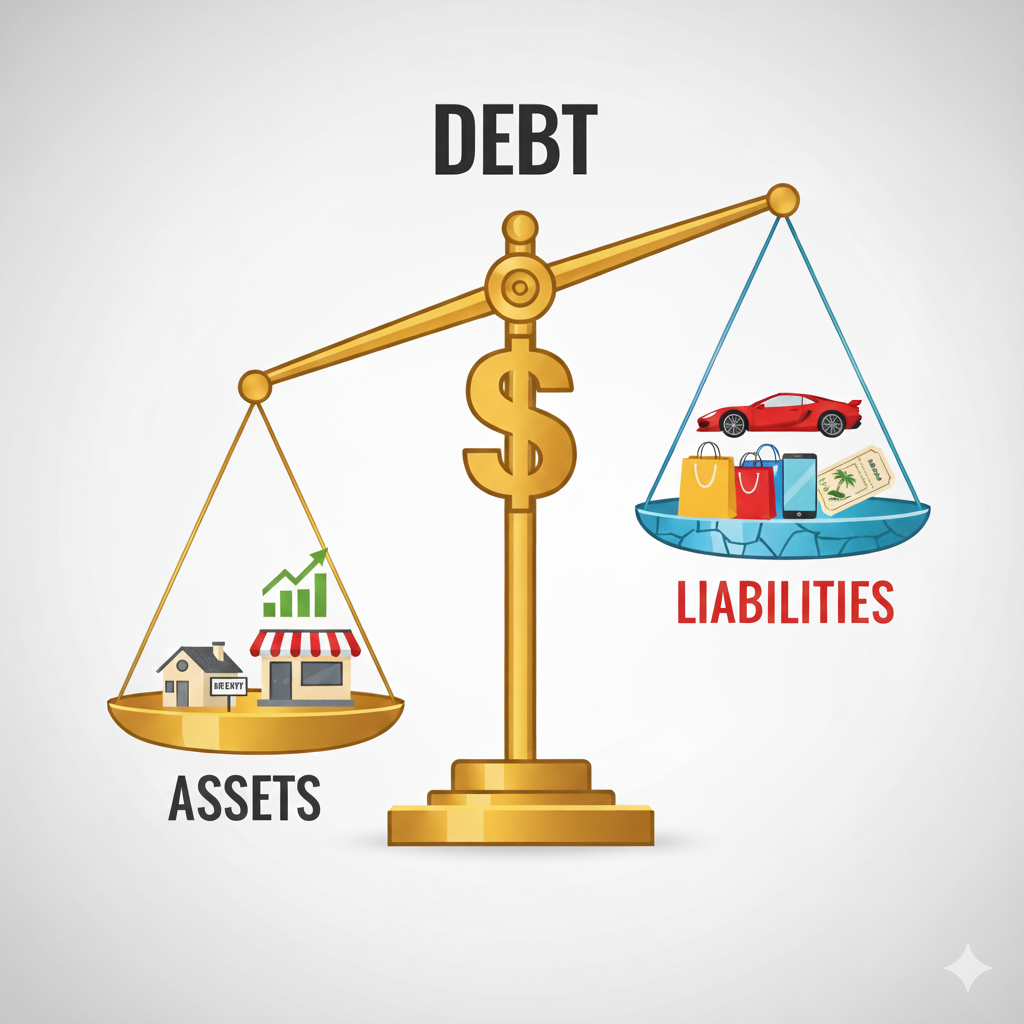

The concept of "good debt" and "bad debt" was famously popularized by Robert Kiyosaki in his book Rich Dad Poor Dad. The distinction is simple but profound. “Good debt puts money in your pocket. Bad debt takes money out of your pocket.”

Bad Debt is money borrowed to buy liabilities. A liability is anything that takes money out of your pocket. Think of high-interest credit card debt used for a vacation, a loan for a brand-new car that loses 20% of its value the moment you drive it off the lot, or personal loans for consumer gadgets. This type of debt makes you poorer.

Good Debt is money borrowed to acquire an asset. An asset is something that puts money into your pocket. This is debt that pays for itself and then some. It’s a strategic tool used to generate income or acquire something that will grow in value.

The core mindset shift is moving from seeing debt as a way to buy things you can't afford to seeing it as a way to finance investments that generate wealth.

The Debt Lifecycle: Are You Built for Leverage?

Financial research on how successful firms use debt reveals a crucial lesson for personal investors: your relationship with leverage should change throughout your life. The "right" amount of debt for you depends heavily on your financial life stage.

- Early Stage (Ages 20-35): In your early career, you have your most valuable asset: time. With a long time horizon and decades of expected income growth, you are better positioned to take on the calculated risks of "good debt." A setback, like a period of rental vacancy or a market dip, is something you have time to recover from. Your higher tolerance for risk allows you to use leverage more aggressively to acquire assets that can grow over 30+ years.

- Mid-Stage (Ages 35-55): During your peak earning years, your focus may shift from aggressive growth to a more balanced approach. You might use leverage to scale your existing asset base, but you'll likely do so more cautiously. You have more to lose, but still enough time to benefit from smart, leveraged investments. This is a period for optimizing and consolidating.

- Late Stage (Ages 55+): As you near retirement, your primary goal becomes capital preservation. Your risk tolerance should be significantly lower. At this stage, taking on new, large debts is often unwise. A major loss could be devastating with little time or earning potential to recover. The focus here is on de-leveraging—paying down existing debts and enjoying the cash flow from the assets you've built.

Putting Good Debt to Work: Real-World Examples

So, how does this look in practice? Here are a few classic examples of using debt to build your asset column.

1. Real Estate Investing

This is the quintessential example of good debt. Imagine you buy a rental property for $250,000. You don't pay for it in cash. Instead, you put down 20% ($50,000) and take out a mortgage for the remaining $200,000.

Your tenant's monthly rent payment covers the mortgage, property taxes, insurance, and maintenance costs. Not only is someone else paying off your loan, but any money left over is positive cash flow directly into your pocket. Meanwhile, the property value is likely appreciating over the long term, building your equity and net worth. You used $50,000 of your own money to control a $250,000 asset. That's the power of leverage.

Of course, real estate carries real risks. Market downturns can erase equity, unexpected vacancies can halt your cash flow, and a major repair can wipe out your profits for a year. It is crucial to do your due diligence and run the numbers carefully. Using tools like a cash-on-cash (CoC) return calculator or a rental property ROI calculator can give you a much clearer picture of your potential profits and risks before you commit.

2. Starting or Buying a Business

Taking out a small business loan can be a powerful form of good debt, but it is arguably one of the riskiest. If a business fails, the loan doesn't just disappear—you're still on the hook for it. Before borrowing, it's critical to have a solid business plan and a clear understanding of your numbers.

Whether you're funding inventory, buying equipment, or acquiring an existing company, you are using borrowed funds to create an engine for cash flow. To do this responsibly, you must project your ability to repay the debt. A business loan calculator can help you estimate monthly payments and total interest costs. Furthermore, understanding your Debt Service Coverage Ratio (DSCR)—a metric lenders use to measure a company's available cash flow to pay its current debt obligations—is vital. A DSCR calculator can help you see if your projected income is strong enough to support the debt. A successful business must generate profits that far exceed these loan payments.

The Golden Rules of Using Debt Wisely

Leverage is a double-edged sword. While it can amplify your gains, it can also magnify your losses. Before you on any debt for an investment, you must do your homework.

Cash Flow is King: The income from the asset must be more than enough to cover the debt payments and all other associated expenses. A negative cash flow investment is a liability, not an asset.

Know Your Numbers: Understand the interest rate, the loan terms, and your total cost of borrowing. Run the numbers for worst-case scenarios, not just best-case ones. What happens if your rental property is vacant for three months or interest rates rise?

Don't Over-Leverage: Using too much debt can leave you vulnerable. If the value of your asset drops, you could owe more than it's worth. Always have a cash cushion and a solid contingency plan.

Focus on Quality: Only borrow to invest in high-quality assets you understand. Whether it's a property in a great location, a business with a proven track record, or a valuable skill, don't let the allure of leverage tempt you into a bad investment.

Your Turn to Reign

Stop thinking of debt as something to be feared and avoided at all costs. Instead, view it as a powerful financial tool waiting to be wielded. Analyze the debt you currently have. Is it buying you assets or liabilities?

By shifting your mindset and your strategy, you can stop being a slave to debt and start making it work for you. That is how you begin to build a financial kingdom that lasts.

Disclaimer: The information provided in this blog post is for educational and informational purposes only and does not constitute financial, investment, or legal advice. The content is not intended to be a substitute for professional advice. All investments, including real estate and business ventures, carry a risk of loss. The use of leverage can amplify both gains and losses. You should not act or refrain from acting on the basis of any content included in this post without seeking the appropriate financial or other professional advice on the particular facts and circumstances at issue from a licensed professional in your jurisdiction. The author and publisher of this post expressly disclaim any and all liability in connection with any action taken or not taken based on any or all of the contents of this blog post.References

- Kiyosaki, Robert. "Learn How to Use Good Debt vs. Bad Debt." Rich Dad, richdad.com.

- O'Brien, Elizabeth. "How to Use Debt to Build Wealth." SmartAsset, 2023, smartasset.com.

- Palmer, Kimberly. "Good Debt vs. Bad Debt: How to Tell the Difference." NerdWallet, 2023, nerdwallet.com.

- U.S. Securities and Exchange Commission. "Leveraged Loan Funds." Investor.gov, investor.gov.